ŌURA ring: Crash test update

ŌURA added AI coaching and blood testing, but can premium pricing survive when all rings track the same metrics?

Earlier this year, we tested the ŌURA Ring Gen 4 and shared our thoughts in a dedicated crash test1. Our verdict was clear: impressive miniaturization and solid execution, but questionable long-term value due to unclear coaching and expensive pricing. Since then, the smart ring market has moved fast enough to warrant an update.

Hardware commoditization

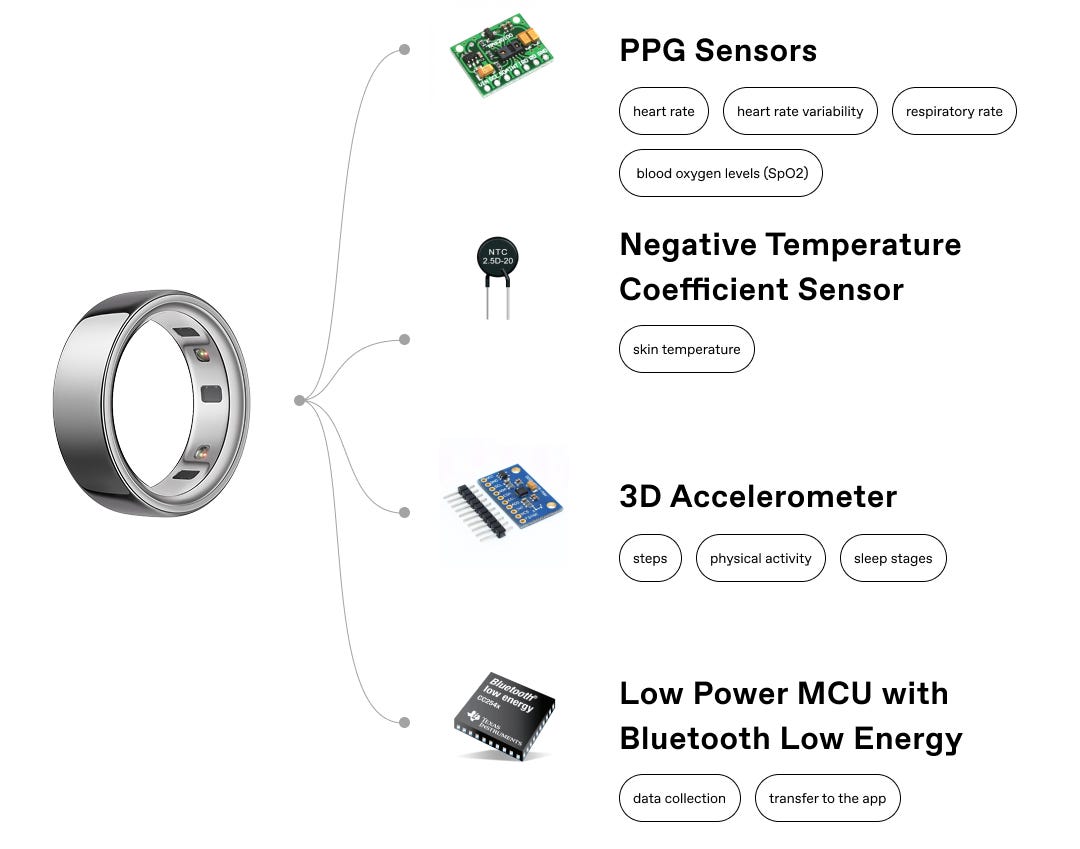

What was once ŌURA’s domain is now a crowded race, the technical barrier to entry has collapsed. Our manufacturing partners in China confirm what the market is showing: smart rings have become commodity hardware. Factories are mass-producing rings with nearly identical sensor configurations (eg. PPG for heart rate, temperature sensors, accelerometers, Bluetooth chips).

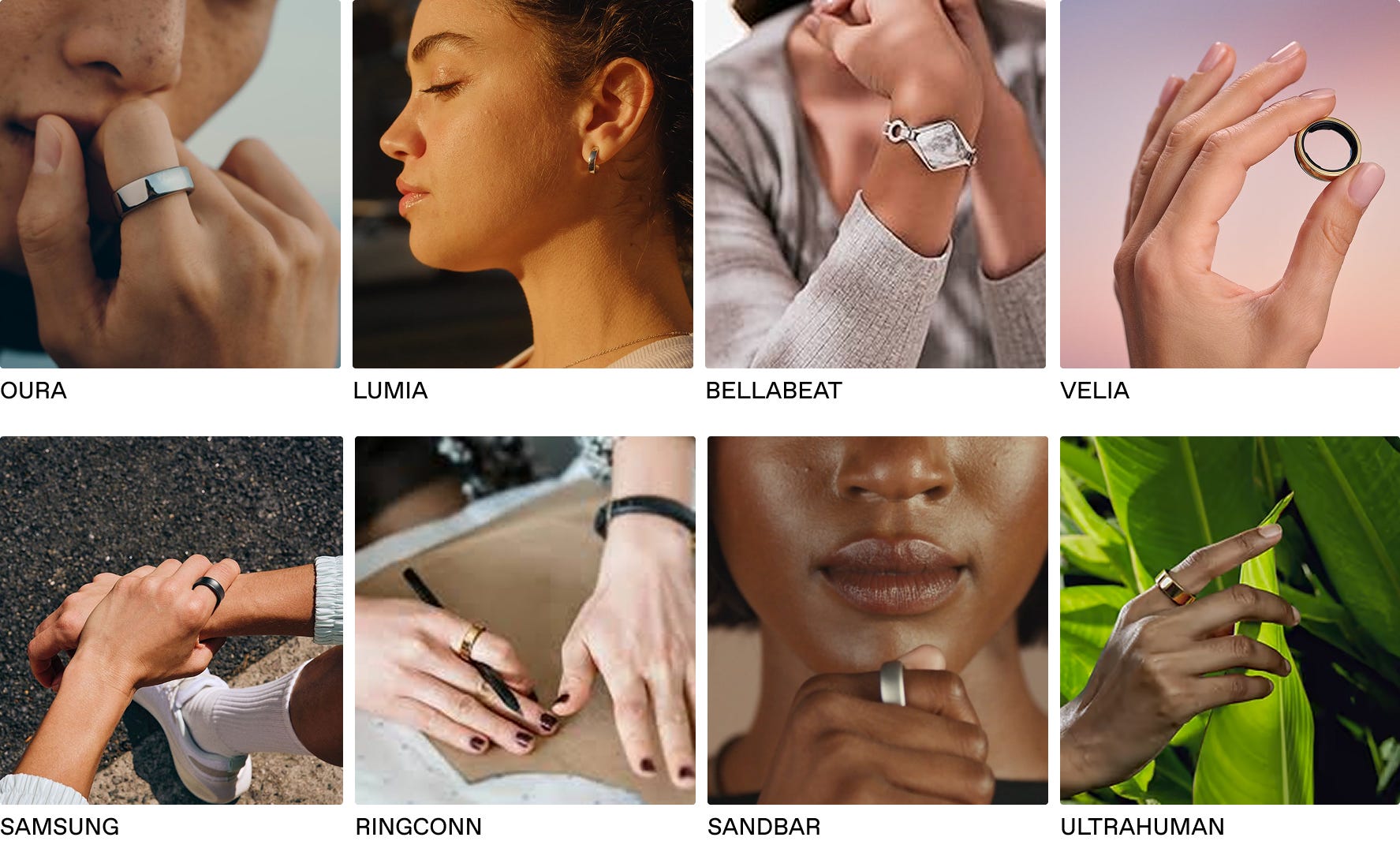

This commoditization creates a fundamental challenge for market leaders. When the hardware becomes undifferentiated, competition shifts to software, ecosystems, and brand positioning. Samsung entered with the Galaxy Ring. Ultrahuman is aggressively pushing a no-subscription model. RingConn offers detailed metrics at lower prices. Even experimental players like Lumia are testing whether earrings can deliver similar biometric value without the downsides of wearing a ring during sports.

ŌURA still leads, but its premium pricing strategy now requires constant justification.

ŌURA leading the race

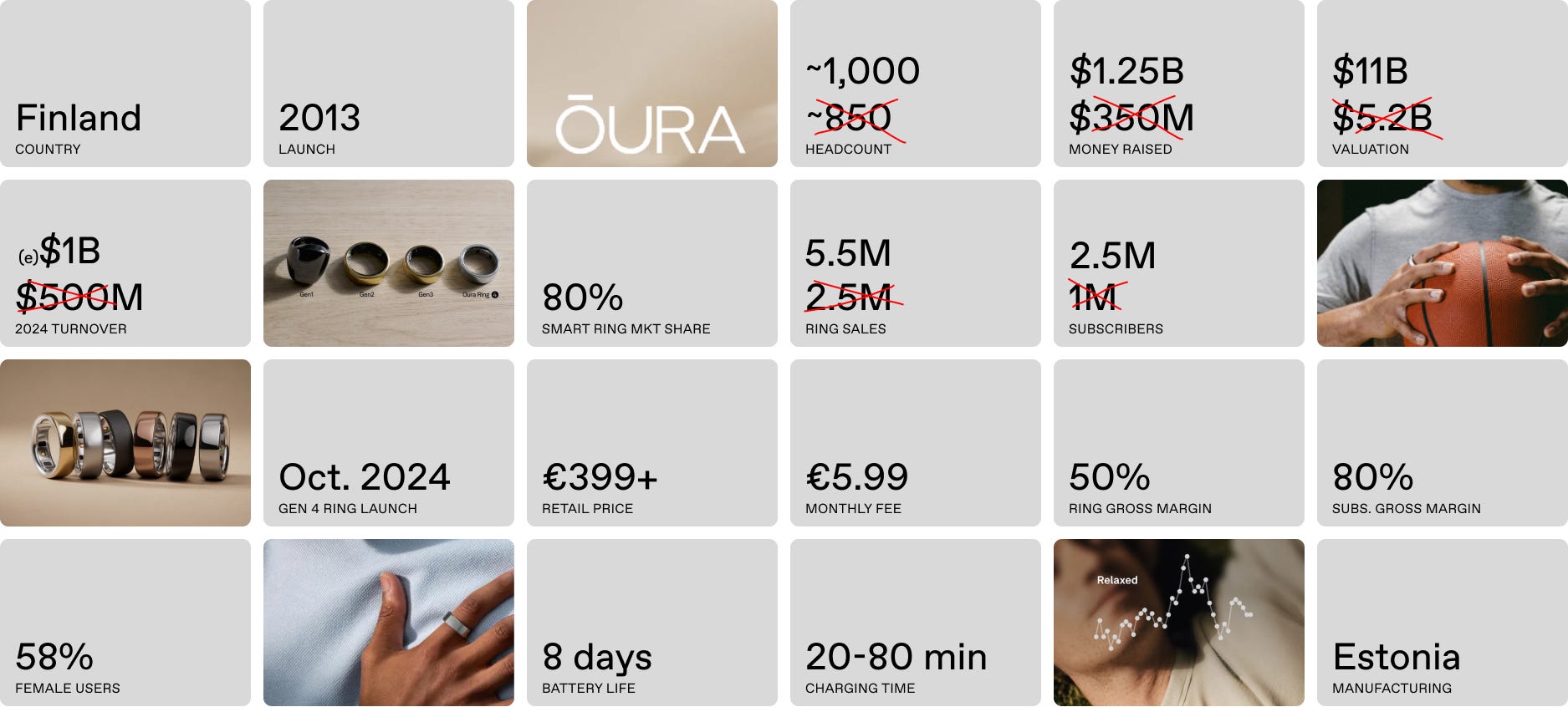

ŌURA’s response has been aggressive. First in expansion, with the company more than doubling its unit sales and active subscribers this year. To fuel this growth, Oura secured a massive $900 million funding round in October 2025. Second, in legal battles around patent infringements2.

These numbers demonstrate that despite increasing competition, ŌURA maintains market leadership, but new entrants are taking bites from different angles.

Strategically, ŌURA now focuses on women in their early twenties. This demographic focus makes sense: a group more willing to invest in preventive health tracking, women-specific features, comfortable with subscription models, and likely to value discrete wearables over bulky smartwatches. But it also highlights the growth challenge: ŌURA needs to continuously find and convert new user segments to sustain its trajectory.

Filling the gaps

ŌURA released features that respond to criticisms we raised in our original test: actionable coaching, not just metrics. Most notably, ŌURA Advisor, an AI-powered health assistant that addresses the “now what?” problem. Instead of just stating “you slept poorly,” it contextualizes: “You’ve had three nights of poor sleep this week, which typically happens when your bedtime shifts. Try going to bed 30 minutes earlier tonight.” Users can customize interaction frequency and tone, avoiding notification spam.

The second addition is Health Panels, a blood testing service via Quest Diagnostics. For $99, members can order comprehensive lab tests covering 50 biomarkers that integrate directly into the ŌURA app. This bridges consumer wearables and clinical healthcare, acknowledging that ring sensors can only measure certain things. By partnering rather than building proprietary hardware, ŌURA creates genuine ecosystem value.

However, accessibility questions emerge. At $400+ for the ring, $6/month subscription, and $99 per blood panel, ŌURA’s complete proposition is expensive. The people who might benefit most from early health intervention are often those least able to afford it.

These additions justify the subscription cost better than Gen 4 did at launch. But the question remains: how many users will sustain this engagement beyond initial novelty?

Competition heats up

Competition is reshaping around four key dimensions:

Ecosystem building: Rings can’t measure everything. Winners will partner strategically rather than cramming more sensors into one device. ŌURA’s Quest partnership and Ultrahuman’s multi-device approach (ring, CGM, blood testing) demonstrate this. No single form factor serves all use cases.

Price justification: As sensors commoditize, price pressure intensifies. The market is splitting between premium positioning justified by software versus affordable hardware for basic tracking. ŌURA must prove their AI coaching, blood testing integration, and brand warrant the premium.

Feature focus: ŌURA’s demographic targeting shows smart strategic thinking. Rather than being everything to everyone, nail specific use cases. Period tracking, fertility insights, and style options create differentiation that matters more than marginal sensor improvements.

Form factor experimentation: The market hasn’t converged on rings as the only answer. Lumia’s earring demonstrates that similar biometric tracking can happen in different form factors that avoid ring-related limitations (eg. gym, bouldering).

AI hype filtering: we see a lot of gimmick products flooding the market betting on various AI-boosted value propositions, however they’ll need to demonstrate real value and long term usage to stay relevant (eg. Sandbar). See our recent AI wearables analysis on the topic.

Conclusion

Six months later, the smart ring market is maturing, technology keeps improving, but key questions ahead:

Will users sustain engagement once the novelty fades, or will smart rings join the graveyard of abandoned fitness trackers?

As platforms collect more intimate health data across devices and lab tests, who actually controls and benefits from this information when companies get acquired or fail?

Can premium players like ŌURA maintain differentiation when hardware commoditizes, or will “good enough” become the market standard?

Industry is optimizing for more tracking, more metrics, more AI insights. But nobody’s proven whether more data actually leads to healthier lives or just more expensive dependencies. The winning product won’t be the one with the most features. It’ll be the one that helps people build lasting health habits and then gets out of the way. Thanks for reading and let us know what you think!

| A guest post by

|